|

Return To Main Page

Contact Us

Rock star Growth Puts Plug Power (NASDAQ:PLUG) In A

Position To Use Debt

Feb 26, 2023

David Iben put it well when he said, 'Volatility is not a risk we care

about. What we care about is avoiding the permanent loss of capital.' So

it might be obvious that you need to consider debt, when you think about

how risky any given stock is, because too much debt can sink a company. We

can see that Plug

Power Inc. (NASDAQ:PLUG)

does use debt in its business. But should shareholders be worried about

its use of debt?

When Is Debt A Problem?

Debt is a tool to help

businesses grow, but if a business is incapable of paying off its lenders,

then it exists at their mercy. In the

worst case scenario, a company can go bankrupt if it cannot pay its

creditors. However, a more usual (but still expensive) situation is where

a company must dilute shareholders at a cheap share price simply to get

debt under control. By replacing dilution, though, debt can be an

extremely good tool for businesses that need capital to invest in growth

at high rates of return. When we think about a company's use of debt, we

first look at cash and debt together.

See our latest analysis for Plug Power

What Is Plug Power's Net Debt?

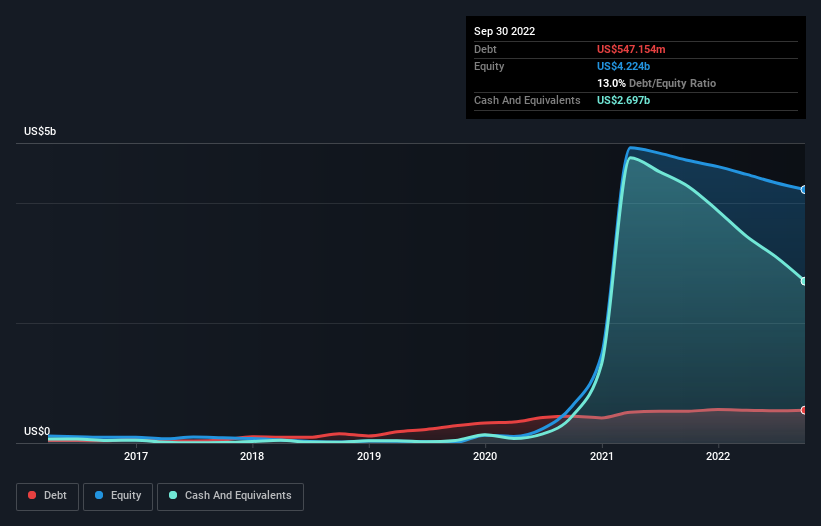

The chart below, which you

can click on for greater detail, shows that Plug Power had US$547.2m in

debt in September 2022; about the same as the year before. But on the

other hand it also has US$2.70b in cash, leading to a US$2.15b net cash

position.

NasdaqCM:PLUG Debt to Equity History February 26th 2023

How Strong Is Plug Power's Balance Sheet?

According to the last

reported balance sheet, Plug Power had liabilities of US$599.4m due within

12 months, and liabilities of US$1.04b due beyond 12 months. Offsetting

these obligations, it had cash of US$2.70b as well as receivables valued

at US$148.9m due within 12 months. So it actually has US$1.21b more liquid

assets than total liabilities.

This short term liquidity is a sign that Plug Power could probably pay off

its debt with ease, as its balance sheet is far from stretched. Simply

put, the fact that Plug Power has more cash than debt is arguably a good

indication that it can manage its debt safely. The balance sheet is

clearly the area to focus on when you are analysing debt. But ultimately

the future profitability of the business will decide if Plug Power can

strengthen its balance sheet over time. So if you want to see what the

professionals think, you might find this

free report on analyst profit forecasts to be interesting.

Over 12 months, Plug Power reported revenue of US$643m, which is a gain of

1,951%, although it did not report any earnings before interest and tax.

When it comes to revenue growth, that's like nailing the game winning

3-pointer!

So How Risky Is Plug Power?

We have no doubt that loss making companies are, in general, riskier than

profitable ones. And the fact is that over the last twelve months Plug

Power lost money at the earnings before interest and tax (EBIT) line. And

over the same period it saw negative free cash outflow of US$956m and

booked a US$693m accounting loss. Given it only has net cash of US$2.15b,

the company may need to raise more capital if it doesn't reach break-even

soon. The good news for shareholders is that Plug Power has dazzling

revenue growth, so there's a very good chance it can boost its free cash

flow in the years to come. High growth pre-profit companies may well be

risky, but they can also offer great rewards. For riskier companies like

Plug Power I always like to keep an eye on the long term profit and

revenue trends. Fortunately, you can click

to see our interactive graph of its profit, revenue, and operating

cashflow.

If you're interested in investing in businesses that can grow profits

without the burden of debt, then check out this free list

of growing businesses that have net cash on the balance sheet.

What are the risks and opportunities for Plug Power?

Have feedback on this article? Concerned about the content? Get

in touch with

us directly. Alternatively,

email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We

provide commentary based on historical data and analyst forecasts only

using an unbiased methodology and our articles are not intended to be

financial advice. It does not constitute a recommendation to buy

or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven

by fundamental data. Note that our analysis may not factor in the latest

price-sensitive company announcements or qualitative material. Simply Wall

St has no position in any stocks mentioned.

Green Play Ammonia, YielderÛ NFuel Energy.

Spokane, Washington. 99212

www.exactrix.com

509 995 1879 cell, Pacific.

Nathan1@greenplayammonia.com

exactrix@exactrix.com

|