|

New US Hydrogen Strategy: Wrong

Department, Wrong Authors

The US

hydrogen strategy was positioned in the wrong federal department. It

was put in the hands of people who deal with fossil fuels all day long

and have a paradigm of burning them for energy, not a paradigm of

electricity for energy. It fails RumeltÆs test for the first thing

that makes a good strategy, and so its principles and actions will be

failures as well.

The US Department of Energy (DOE) is in

an interesting spot in the transformation to a low-carbon economy. 55%

of its budget is for nuclear energy, but most of the USAÆs 100 or so

reactors are aging out and all but a couple will be off the grid by

2035. There certainly arenÆt any plans to build 100 new nuclear

reactors in the States as the country doesnÆt have the conditions for

successful nuclear rollout any more, and the current hope of

SMRs will probably fail to deliver.

While over half of the DOE budget is

focused on nuclear, the USA is realistically going to replace the vast

majority of nuclear generation with renewables, additional

transmission Ś especially

HVDC Ś and storage, just like almost every other country in the

world. All of those technologies are in the DOEÆs remit as well. So

far so good, although the bureaucracy and internal fiefdoms will

undoubtedly be slow to accept this.

But the DOE also deals with fossil fuels as a minority of its

portfolio. It has a large portion of its budget and staff who deal

with coal, oil, and gas. This is likely where part of the problem lies

with its

recently released draft hydrogen strategy.

Given that BidenÆs Inflation Reduction

Act (IRA) has already had a negative impact on European additionality

rules for green hydrogen electrolysis on that continent, itÆs

interesting that the strategy for hydrogen still has wet ink. The

American model is subsidies for manufacturing green hydrogen to bring

its price down closer to black and gray hydrogen, and that money

talked, with major European players making it clear that they would

decamp to the USA. So, grid electricity for hydrogen in Europe, no

requirement to set up PPAs for sufficient wind and solar to cover the

demand. Pity.

So letÆs talk about what a good strategy

is. IÆve read the vast majority of strategy books out there Ś

occupational hazard for a strategist Ś and certainly all the

frequently cited ones or the ones considered important, with the

exception of ClausewitzÆ

On War. There are really only two good broad books on

strategy, Sun Tzu for military matters and for non-military concerns

RumeltÆs

But this assessment is distinctly in the

non-military strategy camp, and so IÆll use RumeltÆs kernel of good

strategies to frame my thoughts on the DOE hydrogen strategy.

ōStrategy is designing a way

to deal with a challenge. A good

strategy, therefore, must identify the challenge to be overcome, and

design a way to overcome it. To do that, the kernel of a good strategy

contains three elements: a diagnosis, a guiding policy, and coherent

action.ö

The diagnosis is the key thing here. What

is going on must be clearly understood. Empirical reality is critical

to good strategy.

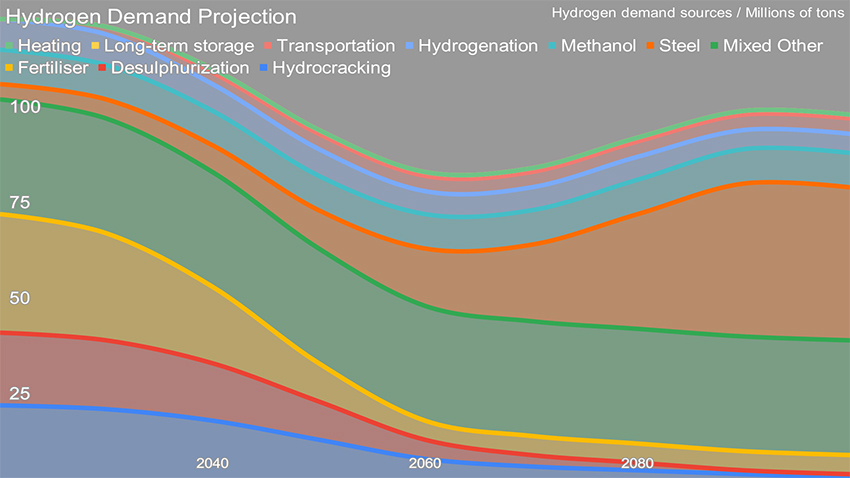

This is my projection of hydrogen demand

through 2100, iterated a few times. I use it to assist major

institutional investors, VCs and renewable deployment organizations to

get their strategy for the coming decade of investments, resourcing

and action plans into the right place.

WhatÆs the most obvious thing about this

projection? Hydrogen demand is shrinking, not growing for much of the

coming decades. Why? Because hydrogen isnÆt a decarbonization

solution, itÆs a global warming problem.

Black and gray hydrogen is a CO2e problem

in the range of all of global aviation. Job one is to stop digging

holes, and hydrogen manufacturing today is a big shovel. ItÆs all from

fossil fuels today, with CO2e emissions from upstream natural and coal

bed methane leakages and CO2 from steam reformation or coal

gasification from 12 to over 35 times the mass of CO2e as hydrogen

manufactured.

And the largest chunk of it is used in

fossil fuel refining, oil refineries to be specific, where itÆs used

mostly to desulphurize heavy crude like AlbertaÆs product and also for

hydrotreating which is used to stabilize desirable aromatics, a much

smaller volume but high value market. ThatÆs about 50 million of the

120 million tons of pure and syngas blended hydrogen we consume today,

or 42%. The second largest chunk is for ammonia-based fertilizers,

about 33 million tons, or around 28%. Refinery use has to mostly go

away if we want to deal seriously with global warming. Ammonia-based

fertilizer use has to diminish radically as well, through the four

trends or strategies of shifting subsistence farmers to urban

employment, precision agriculture, low-tillage agriculture, and

agrigenetics solutions such as

Pivot BioÆs enhanced nitrogen fixing microbes.

Hydrogen is not used for energy today. It

is used in industrial processes to refine energy carriers, and itÆs

used in industrial processes to manufacture fertilizer. The other uses

include hydrogenation of vegetable oil for edible oil products and a

bunch of other things.

But itÆs not a carrier of energy right

now. Which begs the question:

Why is the

US Department of Energy

being tasked with drafting the hydrogen strategy?

The placement of responsibility

presupposes the answer, that hydrogen will be used in the future as a

carrier of energy. And thereÆs little reason to believe that is true.

This makes the DOE a questionable place

to position a hydrogen strategy. By definition, they canÆt help but

view it as an energy carrier. ItÆs their entire paradigm.

It makes more sense to position green

hydrogen as an industrial strategy, something touted by the Biden

Administration as being core to what they are trying to achieve with

their

five-pillar industrial policy. Those pillars are supply chain

resilience, targeted public investment, public procurement, climate

resilience, and equity. ItÆs not bad, with a more balanced perspective

on China than most US governmental material these days.

Putting hydrogen into the DOE was the

wrong choice. The strategy probably should have been in the hands of

the Department of Commerce (DOC), not the Department of Energy, and

the DOC should have asked for input from the DOE and Department of

Transportation (DOT) where appropriate. That ship has sailed, however,

and likely for the usual reasons when it comes to hydrogen, lobbying

from the fossil fuel industry and starting from the wrong paradigm.

And so, thereÆs some good stuff in the

draft and a lot of stuff thatÆs just off base, a bunch of which will

seriously muddle success with decarbonizing hydrogen.

The DOE authors get some of this right.

The first couple of things that they suggest in the demand section,

ōStrategy 1: Target Strategic, High-Impact Uses of Hydrogen,ö make

perfect sense. We use a lot of methanol and ammonia in

industry and agriculture, itÆs all made with black or gray

hydrogen today, and we need to replace that with green hydrogen. And

they point out the potential for the use of hydrogen in steel

making to reduce iron ore instead of coal (without

recognizing the efforts around using electricity directly for that

purpose),

But then they fall off the rails rapidly.

First, they make the common mistake that only burning gases or

liquids can provide high quality heat over 300░ Celsius. This

is an odd mistake when the USA has made 70% of its steel from scrap in

electric steel minimills for a couple of decades, and those use

electric arc furnaces that provide 1,500-3,000░ Celsius high-quality

heat. Similarly, electrically-powered aluminum smelters run at 800░

Celsius. Presumably people in the DOC know this, but the people in the

DOE writing the strategy are oil, gas, and coal heads who assume that

you have to burn gases or liquids for high-quality heat. This just

isnÆt true, and itÆs a major failing in the diagnosis section of the

kernel.

You canÆt get strategy right if you donÆt

start with reality.

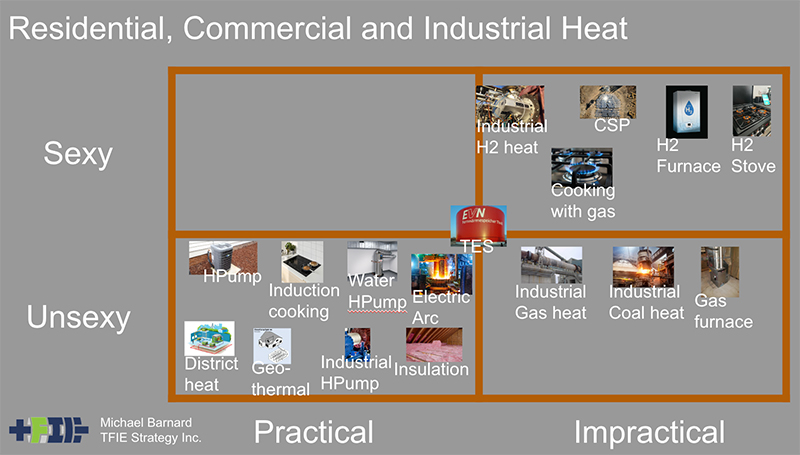

Sexy / Unsexy,

Practical / Impractical quadrant chart for residential, commercial and

industrial heat sources by Michael Barnard, Chief Strategist, TFIE

Strategy Inc.

Heat is important across the economy, but

industrial heat will virtually always be better supplied by

electrically powered solutions in the future. There are a couple

of industrial processes such as cement clinker kilns where I

understand thereÆs a specific value in jets of flame, but those are

the exception, not the rule. An industrial policy from the DOC would

more likely start with the need for heat, and not start with the false

assumption of a requirement for a liquid or gaseous fuel.

As chemical process engineer Paul Martin,

who has been designing modular chemical processing plans for clients

globally for three decades, has told me on a

couple of occasions, everything he does uses electricity up until

the point that cost-benefit analyses show that fossil fuels are

cheaper when the atmosphere is allowed to be used as an open sewer.

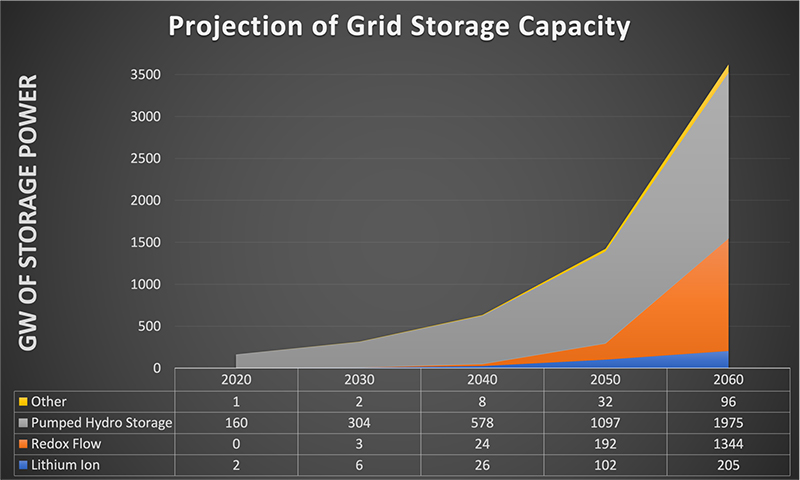

Projection of

grid storage capacity through 2060 by major categories by Michael

Barnard, Chief Strategist, TFIE Strategy Inc.

Then thereÆs hydrogen for

long-duration storage. One of the head-scratchers in my

discussion with Jigar Shah, the DOEÆs director of its Loans

Program Office, was the $504 million loan for a hydrogen salt cavern

storage and electricity generation facility on the site of an old coal

plant in Utah. The assertion was that it reused the transmission to

LA, so it was good. But they are putting gas generation on the site to

replace the coal, that will require a bunch of new gas pipeline to

supply the gas, there is no feeder transmission to the site to bring

renewables to it to manufacture green hydrogen, and green hydrogen is

deeply inefficient round trip. ItÆs what got approved as Utah didnÆt

want the coal town to disappear, but keeping a rural town with a

couple of thousand people alive after its primary economic purpose is

gone isnÆt a strategically sound energy or decarbonization solution.

Like every other major country in the

world, the USA has a lot of grid storage today in the form of pumped

hydro. That technology is by far the biggest form of grid storage in

the world, itÆs by far the largest form of grid storage under

construction, and single pumped hydro facilities commissioned in 2022

dwarf all battery storage on the grid globally. ItÆs the appropriate

scale and technology for grid storage. Hydrogen is just a bad

technology by comparison for this purpose.

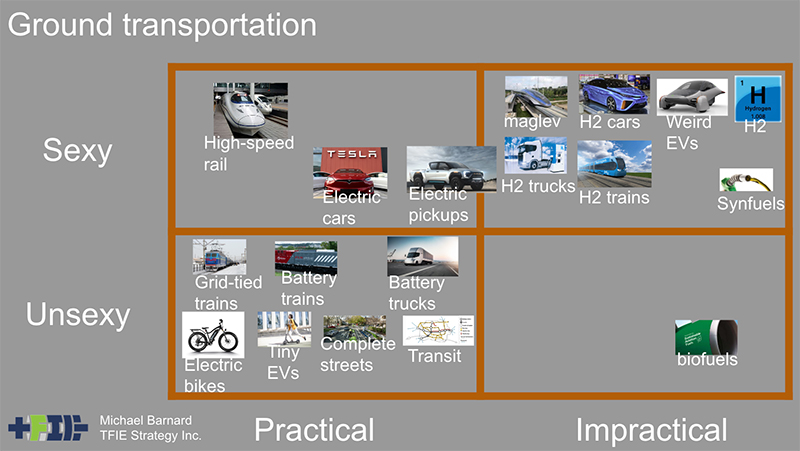

Then thereÆs

hydrogen and synthetic fuels for trucks and buses, also

touted in the DOE strategy. This in a world where there are 500,000

battery-electric buses on the roads of China, where there are roughly

the same number of battery electric trucks, where new battery-electric

semis are being delivered from multiple manufacturers today, and where

every hydrogen bus and truck test program has proven that they are not

economic compared to battery-electric, with potential en route grid

ties or inductive charging in places.

You have to be looking at

the world through diesel-powered glasses to assume that burning gases

or liquids in trucks and buses is an appropriate choice in a strategy

when battery-electric is an option. Synthetic fuels are much higher

CO2e and much higher cost. ItÆs mostly just economics, and fuel costs

are about 21% of the costs of trucking. I assessed this end-to-end in

2018 and 2019 in looking at

Carbon EngineeringÆs direct-air capture air-to-fuel plans, and the

economics and technology have not budged since then.

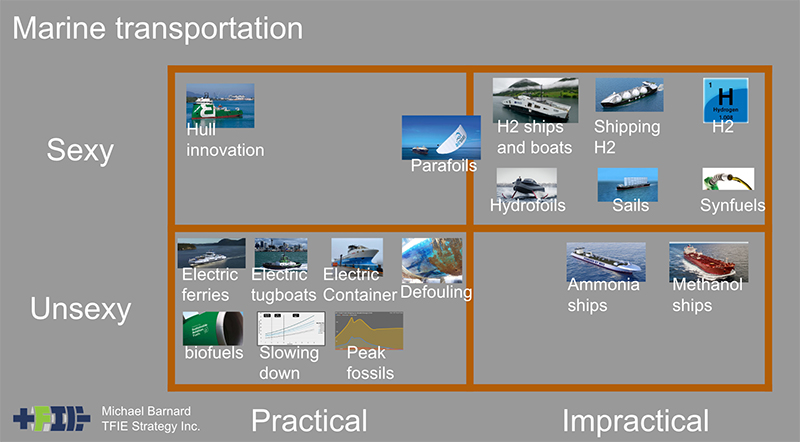

Sexy/unsexy, practical/impractical

quadrant chart of marine transportation decarbonization by Michael

Barnard, Chief Strategist, TFIE Strategy Inc.

ThereÆs a different story in

marine transportation, another target for hydrogen in the DOE strategy.

Perhaps if the strategy originated in the Department of

Transportation, which is responsible for marine shipping, there would

be some reasonable material here. However, there are many, such as

Maersk, who are trying to square the circle of synthetic fuels

manufactured from green hydrogen, so perhaps not.

There are a few key points itÆs possible

that the DOE authors donÆt know. The first is that 40% of all

deepwater shipping is for bulk oil, gas, and coal shipments between

continents. ThatÆs all going away. Next is that 15% of all deepwater

shipping is for raw iron ore, heading to the same ports as a lot of

the coal to manufacture steel. ThatÆs going to be significantly

reduced. Other bulk goods such as grains are already containerizing.

The target is container shipping and itÆs smaller, in other words.

Next, the question as always is how much

of shipping can electrify. The answer is that all inland shipping and

about two-thirds of near shore shipping can run on batteries, either

permanently installed in the boats and charged as

Corvus Energy has been doing for over a decade, or by putting the

batteries in standard shipping containers (TEU) and swapping them out

in ports, a solution also suitable for trains which IÆll be coming to.

TEUs with batteries installed are already being delivered globally for

grid storage by Tesla and Wõrtsilõ, as I discussed with the latter

companyÆs

global VP for energy storage and optimization, Andy Tang, a few

months ago.

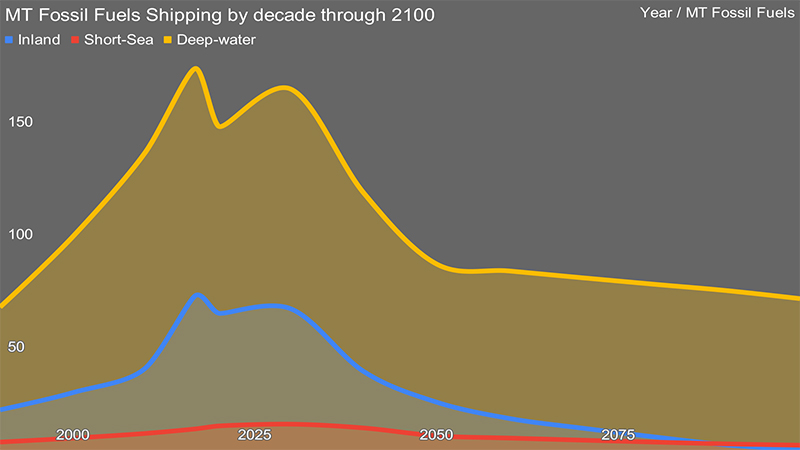

Marine shipping megatonnes fossil

fuels before refueling, chart by Michael Barnard, Chief Strategist,

TFIE Strategy Inc.

That only leaves the

declining deepwater shipping segment that requires a solution, and it

is deeply unlikely to be hydrogen or synthetic fuels. In my assessment

of alternative fuels for marine shipping, I settled on biofuels as the

highest probability for the dominant solution. My projection of marine

energy requirements for that space through 2100 makes it clear that

global carrying capacity of stalk cellulosic biofuels is more than

enough for the actually hard to refuel long haul segments of both

aviation and shipping.

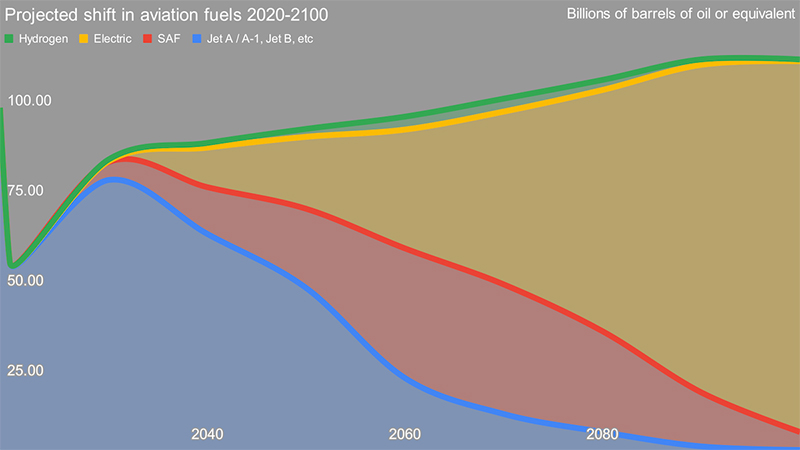

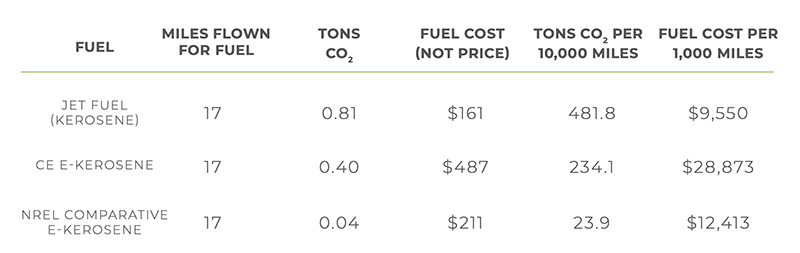

Projection of aviation fuel demand

by type through 2100 by Michael Barnard, Chief Strategist, TFIE

Strategy Inc.

And so, to aviation,

another area the DOE thinks is a target for green hydrogen demand.

From the same Carbon Engineering assessment cited above, and in my

assessments of refueling options for that segment of transportation,

itÆs clear that hydrogen is not fit for purpose directly, and

synthetic fuels will be much more expensive than SAF biofuels.

Table from Carbon Engineering

synthetic fuel case study by Michael Barnard, Chief Strategist, TFIE

Strategy Inc.

What cannot be electrified with

ever-improving batteries will use SAF biofuels. TheyÆve been around

since 2011, most aerospace OEMs are certifying their aircraft on them,

and they are flying blended or solely SAF biofuels in test routes with

real cargo and passengers today. But as the table shows, as long as

Jet A-1 and the like are cheaper, thatÆs what aviation will use.

Thankfully thatÆs changing in multiple parts of the world as the

weird untaxed condition of jet fuels ends, something I explored a

few months ago.

And then thereÆs rail, another

target the DOE strategy considers to be high value. China has

built

25,000 miles of high-speed, grid-tied, electrified freight and

passenger rail in the past 15 years, reaching 93% of domestic

cities, and itÆs connecting neighboring countries into the network.

Germany just announced that it will not build any more hydrogen rail

after the 50-mile test route, as economic studies show itÆs 3 times as

expensive as grid-tied/battery hybrid, and almost that much more

expensive than just battery-electric. All freight train engines in the

USA are already diesel-electric hybrid, and grid-tying them with

overhead lines is a common practice globally.

Once again, those battery-filled TEUs are

perfect components for a battery-electric train system, rechargeable

at existing transshipment points, where the

cranes are going all electric as well. Having had CN Rail as a

client a decade ago, looked at global container shipping, and looked

at container port management software, itÆs relatively trivial to have

TEUs filled with batteries charging in container transshipment

facilities and dropped onto waiting train cars or into the holds of

container vessels.

Finally, the strategy references

residential and commercial heating as a target for hydrogen.

IÆve explored this (see the heating quadrant chart above), as have

dozens of others, and hydrogen would be both

vastly more expensive than natural gas heating and

much less safe. When air, ground, and water-sourced

heat pumps are already refueling very large commercial and

residential buildings, running with coefficients of performance of 3

to 5, being built in gigafactories in Texas, and no hydrogen furnaces

or stoves for residential or commercial use are available for purchase

or certified for use, you really have to want to burn something to

consider hydrogen as an alternative.

I might return to this to address the

wrong-headed assumptions regarding the need to transport hydrogen by

pipeline, rail and ship, another set of paradigm errors the DOE

strategy makes. Suffice it to say that virtually all hydrogen is

manufactured at point of demand today because itÆs so difficult and

expensive to transport, and that its low energy density by volume and

tiny molecular size means that itÆs very expensive to transport more

than a few hundred meters. IÆve assessed

pipeline and

shipping costs for hydrogen, and they make no sense compared to

putting renewable electricity into HVDC lines, a common technology

globally, with a third undersea HVDC interconnector going in in the

UK, tens of thousands of kilometers of HVDC in China, Morocco to UK

HVDC under construction, and Australia to Singapore HVDC proposed.

The future of energy transmission is

electricity flowing down high voltage direct and alternating current

lines, not moving molecules.

The reason that the DOE strategy, if it

persists in this form, will be so problematic for the USA is that it

first diffuses the attention of hydrogen as a decarbonization problem,

so it wonÆt be addressed promptly. Second, itÆs going to cause a lot

of organizations to waste a lot of time and money building

infrastructure to manufacture hydrogen in locations where there will

be no demand. In some cases, the hydrogen will be able to be

repurposed for high-value uses such as ammonia-based fertilizers. But

in a lot of cases, it will simply be an expensive white elephant and

moved at great expense to someplace more useful.

So why is the USA making this obviously

poor choice? Why is hydrogen positioned in the DOE as opposed to the

DOC? Why are all of these clearly dead-end use cases considered to be

ōStrategic, High-Impact Uses of Hydrogen,ö as the DOE strategy

asserts?

Well, the fossil fuel industry and

governments with large tax and royalty revenues are lobbying hard to

make hydrogen a æreplacementÆ for fossil fuels. They know that unless

hydrogen does the heavy lifting, their fossil fuel reserves have zero

economic value. As

Michael Liebreich likes to point out, the fossil fuel industry

canÆt lose by pushing hydrogen. TheyÆll either delay real climate

action, or theyÆll get a lot of governmental money to make blue

hydrogen out of their fossil fuel reserves.

Oh, did I mention the US DOE hydrogen

strategy is also all over manufacturing hydrogen from fossil fuels

with carbon capture and storage bolted on? Are you surprised?

The US hydrogen strategy was positioned

in the wrong federal department due to the wrong framing. It was put

in the hands of people who deal with fossil fuels all day long and

have a paradigm of burning them for energy, not a paradigm of

electricity for energy. It fails RumeltÆs test for the first thing

that makes a good strategy, acceptance of empirical reality, and so

its principles and actions will be failures as well.

The USA should go back to the drawing

board, and quickly. IÆd be happy to assist them.

Green Play AmmoniaÖ, Yielder« NFuel Energy.

Spokane, Washington. 99212

www.exactrix.com

509 995 1879 cell, Pacific.

exactrix@exactrix.com

|