|

Oil Traders Are Daring to Defy Market Kingpin Saudi

Arabia

-

Price

reaction to OPEC+ output cuts becoming less pronounced

-

Market is closely watching for

signs of a Chinese slowdown

June

11,

2023

By

Alex Longley

Prince Abdulaziz bin Salman al-Saud in Riyadh, on June

11.

Photographer: Fayez Nureldine/AFP/Getty Images

Oil traders are starting to ignore the most important person in the

market. It could prove a risky gambit.

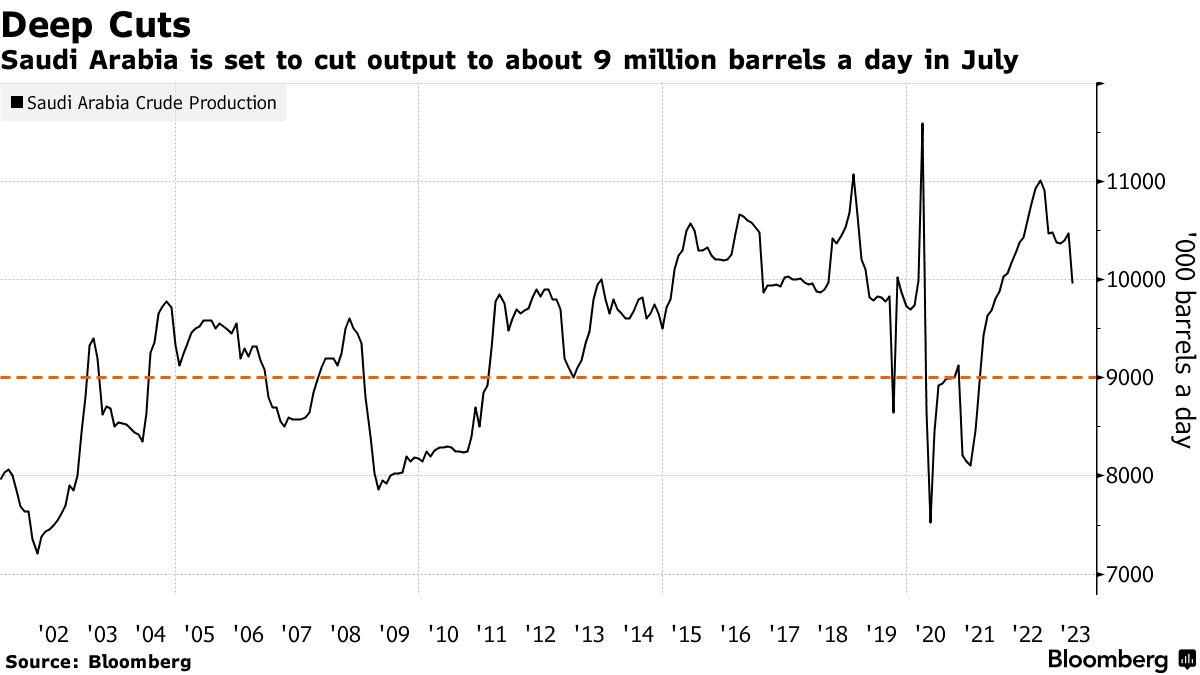

A week ago, Saudi Arabian Energy Minister Prince Abdulaziz bin Salman

pledged to unilaterally cut the country�s July oil production to the

lowest in over a decade, excluding Covid-19 era curtailments. He

described the move as a �lollipop.�

While there�ve been bigger output cuts in recent

months, its symbolism was important, and Prince Abdulaziz left open

the possibility of extending the curb. It also came on the back of a

litany of comments that suggest the prince wants to hurt those who

speculate on lower prices.

Yet, traders are becoming less responsive. The immediate price gain

from the curbs he announced on last Sunday lasted a day. By Friday at

5 p.m. in London, Brent futures were around $76 a barrel � almost

exactly where they were a week earlier. A previous output cut in April

took less than a month to wear off on prices.

Speaking on Sunday, the prince said the OPEC+ agreement was about

being proactive and precautionary. �I think the physical market is

telling us something and the futures market is telling us something

else,� he said at the Arab, China Business Conference in Riyadh. �To

understand OPEC+ today, it�s all about being proactive, preemptive and

precautionary.�

Despite expectations that oil demand will outstrip supply in the

coming months, several things are fueling the bears� confidence. Two

negatives really stand out: the first is that Russian shipments have

boomed in the face of expectations that western sanctions would

curtail them. The second is concern about the fate of China�s economy,

for years the bedrock of demand growth.

�There are many uncertainties, as usual, when it

comes to the oil markets, and if I have to pick the most important one

it�s China,� Fatih Birol, executive director at the International

Energy Agency, said in a Bloomberg TV interview. �If the Chinese

economy weakens, or grows much lower than many international economic

institutions believe, of course this can lead to bearish sentiment.�

Goldman Sachs Group Inc. made its third downward

price revision for the global benchmark in six months, trimming its

Brent forecast for December to $86 a barrel, versus its previous

estimate of $95 a barrel, on rising supplies and waning demand.

.png)

China�s Purchasing Manufacturing Index fell to

48.8 last month, a level that undershot expectations and was also the

weakest reading since December, when the country was mired in Covid

Zero restrictions.

Even if its economy does accelerate anew, China will have a lot of

crude to use up. The country�s stockpiles rose to a two-year high in

May and several traders said they see recent Saudi oil price hikes to

Asia, alongside continued OPEC+ production cuts, as part of an effort

to drain that inventory.

Global Picture

That is compounding a less-rosy � but far from outright bearish �

picture of global demand.

Since January, the IEA � whose supply and demand balances serve as a

benchmark for the world�s oil analysts � has shaved its anticipated

demand increase from second to fourth quarters by 900,000 barrels a

day. It still expects it to expand by a robust 1.8 million barrels a

day, though some are dubious of whether it can be achieved.

Beyond China, there is a global concern about

industrial production, a close proxy for diesel demand. Manufacturing

has been in contraction worldwide for each of the last nine months,

according to JPMorgan data, while a gauge of US trucking is at the

weakest since September 2021. Last week, the US cut its outlook for

consumption of the road fuel.

Those dynamics are, perhaps, part of why the cuts by Saudi Arabia and

its OPEC+ allies are having less of an impact.

�The producer group is in a multiple bind: demand is looking weaker

and non-OPEC supply stronger by year-end than many analysts had

forecast,� Citigroup Inc. analysts including Francesco Martoccia

wrote. �Both OPEC and IEA forecasts have had an air of wishful

thinking about accelerating demand growth.�

Sea Flows

Stubbornly high oil flows are not helping.

While they have slipped in the past few months, observed seaborne oil

shipments are still up sharply compared with where they were in May

2022, a month when Chinese buying was being undermined by the

country�s efforts to contain Covid.

Tracking by Bloomberg shows shipments from the

bulk of the world�s exporters were up 1.13 million barrels a day year

on year. Russia�s cargoes, in particular, are soaring. The nation�s

crude exports were within 100,000 barrels a day of a record in the

four weeks to June 4, according to data compiled by Bloomberg.

That has led to a torpor in the face of supply cuts. Likewise, markets

for physical barrels are � for now at least � showing little sign of

major tightness, though there�s still a month before Saudi Arabia�s

cut takes effect. US crude oil was last week sold in Europe at the

weakest in a month. Prior cuts by some members of OPEC+ began in May.

Risky Position

Despite all that, it�s far from a risk-free bet for the bears.

With the kingdom effectively backstopping any decline in prices, some

investors remain hopeful of meaningful market tightening in the second

half of the year.

China�s Unipec bought oil from the US and Norway last week, a possible

sign that OPEC+�s moves will boost buying of cargoes in other markets

and tighten them up. Indonesia�s PT Pertamina also plowed into the

market, snapping up millions of barrels of west African oil.

Booming oil refining capacity in China and the Middle East looks set

to come up against a �structural dearth of crude in the coming years,�

Saad Rahim, chief economist of trading giant Trafigura Group, said in

the company�s interim report.

The supply cuts by OPEC+, coupled with emerging market demand growth,

should lead to �material draws in inventories later this year� he

said, adding that US shale may not be able to balance the market.

But even if the market does turn, it may take time to filter through,

as traders continue to wrestle with the slew of economic concerns and

robust supplies that have hobbled prices for months now.

�No one wants to take risk in flat price given the macro uncertainty,�

said Richard Jones, an analyst at consultant Energy Aspects.

�Ultimately they are waiting to see physical markets tighten as the

cuts take effect.�

� With assistance by Grant Smith, Yongchang Chin and

Andrew Janes

Green Play Ammonia�, Yielder� NFuel Energy.

Spokane, Washington. 99212

www.exactrix.com

509 995 1879 cell, Pacific.

exactrix@exactrix.com

|